Canadian business owners often accumulate retained earnings inside their corporations. Learn how corporate estate planning and life insurance can help transfer that wealth tax efficiently.

Preserving Corporate Wealth for the Next Generation

A Professional Services Estate Planning Case Study

Client Profile

Andrew Collins is the founder of a Toronto-based engineering consulting firm specializing in structural design and project advisory for commercial and mid-rise developments across Ontario.

Asset Structure

Projected Estate Tax Exposure

Upon Andrew’s death, his shares in OpCo and Holdco would be deemed disposed of at fair market value. Modeled capital gains tax exposure resulted in an estimated estate tax liability of approximately $2.5M.

The issue was not investment performance.

The issue was liquidity and tax efficiency.

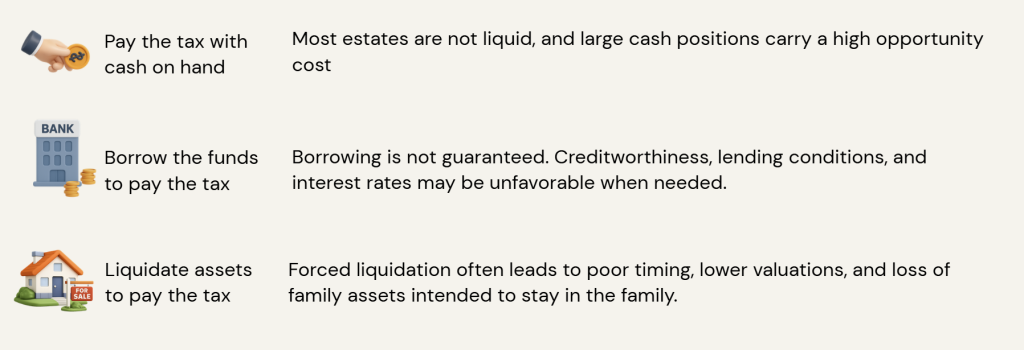

Without planning, the estate would likely need to sell corporate investments or business assets to generate the cash required to pay the tax liability.

The Retained Earnings Challenge

Many successful business owners accumulate significant retained earnings inside a holding company.

Over time, these funds are invested into:

While this allows capital to grow tax-efficiently inside the corporation, it creates a structural problem.

Corporate money eventually needs to become personal money.

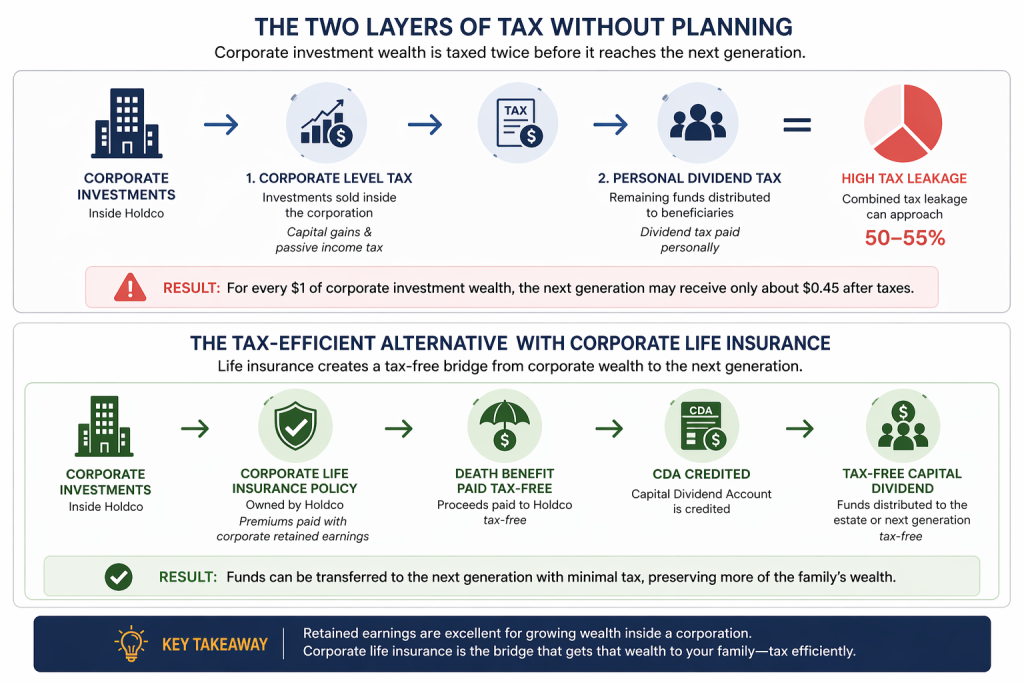

When corporate investment assets are eventually transferred to the next generation, two levels of tax typically apply.

The Two Layers of Tax

In Ontario, the combined tax leakage can approach 50–55%.

This means that for every $1 of corporate investment wealth, the next generation may receive only about $0.45 after taxes.

The Strategy

After reviewing multiple planning scenarios, the advisory team implemented a Holdco-owned participating whole life insurance policy.

The objective was to convert a portion of retained corporate capital into tax-efficient estate liquidity.

Structure Overview

What Happens at Death

Upon Andrew’s passing:

The investment portfolio and business assets remain intact.

The estate does not need to liquidate investments during unfavorable market conditions.

Why This Strategy Worked

The Traditional Alternatives

Working with Estately Wealth

We partner with Canadian accountants and business owners to design advanced estate planning strategies that preserve corporate wealth and improve intergenerational wealth transfer.