Client Profile

David and Priya Mehta are the founders of a 28-year-old Ontario-based manufacturing company specializing in custom metal fabrication for industrial and infrastructure clients across Southern Ontario.

Asset Structure

•

Principal Residence (Personally Held)

•

Operating Company (OpCo)

•

Holding Company (Holdco)

Projected Estate Tax Exposure

Upon death, David and Priya’s shares in OpCo and Holdco would be deemed disposed of at fair market value.

Modeled capital gains and corporate tax exposure resulted in an estimated estate tax liability of approximately $2.9M.

The issue was not asset value. It was liquidity.

The Challenge

1. Significant Tax Exposure

The majority of the family’s wealth was embedded in productive assets:

The deemed disposition of shares at death would trigger an estimated $2.9M tax liability.

2. Cash Flow and Working Capital Constraints

The business required:

Selling assets or using retained earnings would:

Using corporate liquidity to pre-fund the problem would come at the expense of growth and flexibility.

3. Legacy and Family Continuity

One child was active in the business, while one was not involved. The founders’ objectives were clear:

The IFA Solution

After modeling multiple scenarios, the advisory team implemented a corporate-owned permanent life insurance strategy structured as an Immediate Financing Arrangement (IFA).

Structure Overview

At Death

Insurance proceeds would be paid tax-free to Holdco. The Capital Dividend Account would be credited. Tax-free capital dividends could be paid to the estate. The $2.9M tax liability could be funded without selling the business. The loan would be repaid using insurance proceeds, and the operating company would remain intact.

Why the IFA Was Ideal

1.

2.

3.

4.

This structure helped create estate liquidity without forcing the sale of the business.

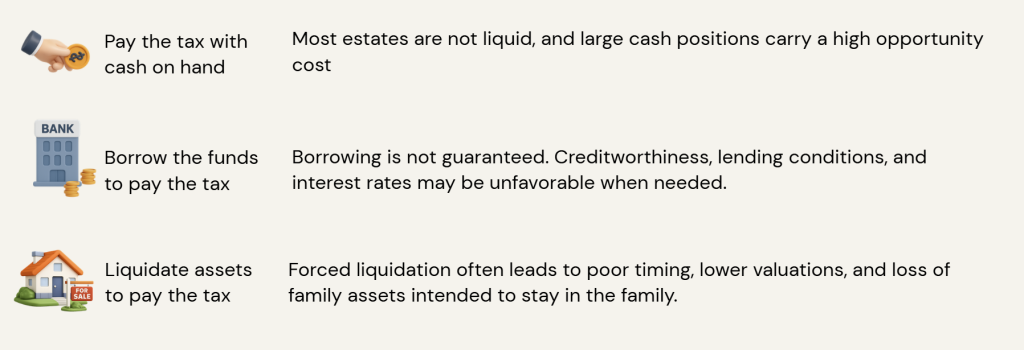

The Traditional Alternatives

Most estates are not liquid, and large cash positions carry a high opportunity cost.

Borrowing is not guaranteed. Creditworthiness, lending conditions, and interest rates may be unfavorable when needed.

Forced liquidation often leads to poor timing, lower valuations, and loss of family assets intended to stay in the family.

The Traditional Alternatives

Working with Estately Wealth

We partner with Canadian accountants to design and implement advanced insurance-based planning strategies.

Working with Estately Wealth

Estately Wealth partners with Canadian accountants and advisors to design and implement advanced insurance-based planning strategies for business owners and professionals.

We support the planning process with technical expertise, structured analysis, and clear documentation, helping ensure complex strategies like IFAs are implemented correctly and integrated into the broader tax and estate plan.